Despite the prevalence of industrial policies around the world, few empirical studies directly evaluate their welfare consequences. This column reveals that the scale of China’s industrial policy targeting the shipbuilding industry is massive, with the lion’s share going to entry subsidies. The effectiveness of different policy instruments is mixed, and the efficacy of industrial policy is significantly affected by the presence of boom and bust cycles, and by heterogeneity in firm efficiency. The ‘white list’ of firms chosen for government support did not include the most efficient firms.

Industrial policies, broadly defined as a policy agenda that shapes a country’s or region’s industrial structure by either promoting or restricting specific sectors, have been widely used in developed and developing countries. Historical examples include the US and Europe after WWII, Japan in the 1950s and 1960s, and South Korea and Taiwan in the 1960s and 1970s. Today, industrial policy in the form of protectionism is once again at the forefront of economic policy in both the East and West. As Rodrik (2010) puts it, “[t]he real question about industrial policy is not whether it should be practiced, but how”.

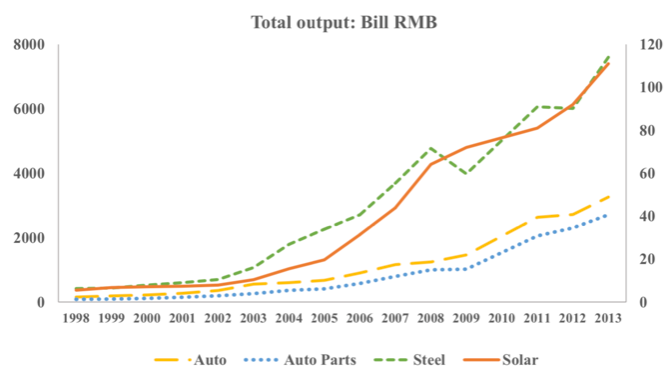

Despite the prevalence of industrial policies in practice and the contentious debate in the literature regarding their efficacy (Baldwin 1969, Krueger 1990), remarkably few empirical studies directly evaluate the welfare implications of these policies. In our recent paper (Barwick et al. 2019), we address this issue with a focus on China, where the regulatory agency has considerable influence over its industries and the ‘invisible hand’ of the state is gaining ground by the day. During the past two decades or so, Chinese firms have rapidly dominated many global industries, such as steel, auto, and solar panels (Figure 1). In recent years, the government is explicitly targeting high-tech sectors to turn its firms into world leaders (‘Made in China 2025’).

Figure 1 Output of Chinese auto, auto parts, steel, and solar industries, 1998-2013

Note: The output of the auto, auto parts and steel industries are plotted on the left-hand vertical axis; the output of the solar industry is plotted on the right-hand vertical axis.

We use the shipbuilding industry as a case study. At the turn of the century, China’s nascent shipbuilding industry accounted for less than 10% of world production. During the 11th (2006-2010) and 12th (2011-2015) national five-year plans, it was dubbed a pillar industry in need of special oversight and support. Since then, an unprecedented number of national policies were issued to develop this infant industry into the largest worldwide. The policies set specific output and capacity goals and as such involved a mix of production, investment, and firm entry subsidies. Production subsidies included input material and export credits, buyer financing, and so on.

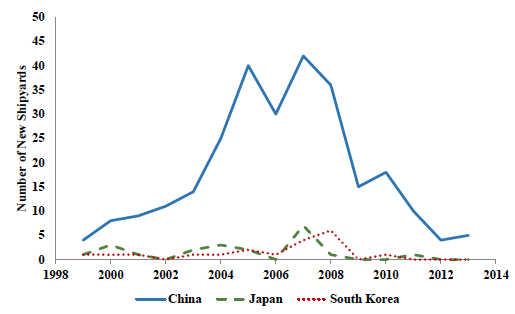

Investment subsidies took the form of low-interest long-term loans and expedited capital depreciation. Finally, reduced processing time and simplified licensing procedures, as well as heavily subsidised land prices significantly lowered the cost of entry for potential shipyards. Within a few years, China overtook Japan and South Korea and became the leading ship producer in terms of output. The industry’s rapid expansion is depicted in Figures 2 and 3. In the aftermath of the 2008 economic crisis and amid a sharp decline in global ship prices, the government then promoted consolidation policies to create large successful firms that can compete against international conglomerates.

Figure 2 Market shares of China, Japan, and South Korea, shipbuilding, 1998-2014

Figure 3 Number of new shipyards in China, Japan, and South Korea, 1998-2014

Using this historical event as a case study, we examine the welfare consequences of industry policies, focusing on three questions of general interest. First, how has China’s industrial policy shaped its domestic and the global industry? Second, what are the welfare consequences of this policy? Third, what is the relative efficacy of different policy instruments, such as production subsidies, investment subsidies, entry subsidies, and consolidation policies?

Our analysis delivers four sets of main findings. First, like many other policies unleashed by China’s central government in the past few decades, the scale of the industrial policy in the shipbuilding industry is massive (relative to the size of the sector), with the lion’s share going to entry subsidies. Our estimates suggest that the aggregate policy support from 2006 to 2013 is equivalent to RMB 550 billion (in nominal terms), with entry subsidies around RMB 330 billion, followed by production subsidies of RMB 159 billion and investment subsidies of RMB 51 billion.

The policy boosted China’s domestic investment and entry by 270% and 200%, respectively, and increased its world market share by 40%, three-quarters of which occurred via business stealing from rival countries. However, contrary to media reports that hailed this as a success, the policy created sizable welfare distortions and generated mediocre net profit gains to domestic producers.

Much of the subsidies were dissipated through the entry and expansion of unproductive and inefficient producers, which exacerbated the extent of excess capacity and did not translate into significantly higher industry profits over the long run.

Second, the effectiveness of different policy instruments is mixed. Production and investment subsidies can be justified on the grounds of revenue considerations, but entry subsidies are wasteful and lead to increased industry fragmentation and idleness. Specifically, entry subsidies attract small and high-cost producers. In contrast, production and investment subsidies favour large and efficient firms that benefit from economies of scale. Production subsidies are more effective at achieving output targets, while investment subsidies are less distorting over the long run. In addition, welfare losses are ‘convex’ in that the combination of multiple subsidies induces firms to make further suboptimal decisions and yields returns that are considerably lower than each policy in isolation.

Third, our analysis suggests that the efficacy of industrial policy is significantly affected by the presence of boom and bust cycles, as well as by heterogeneity in firm efficiency, both of which are essential features of the shipbuilding industry. A counter-cyclical policy would have out-performed the pro-cyclical policy that was adopted by a large margin where the effectiveness of raising long-run industry profit differs by nearly threefold. This is partly due to a composition effect (more high-cost firms survive during a boom than during a bust), and partly due to capacity constraints that render increases in production more costly during the boom. In a similar vein, had the government targeted subsidies towards more efficient firms, the policy distortions would have been considerably lower.

Fourth, we examine the consolidation policy adopted in the aftermath of the financial crisis, whereby the government implemented a moratorium on entry and issued a ‘white list’ of firms chosen for government support. This strategy was adopted in several industries to curb excess capacity and create large conglomerates that can compete globally (see Yap and Mazur 2013 for an example). Consistent with the evidence discussed above, we find that targeting low-cost firms creates fewer distortions. That said, the ‘white list’ released by the government favoured state-owned enterprises and did not include the most efficient firms. Finally, the profit gains of a policy package that involves entry subsidies (to overcome entry barriers and capital market inefficiencies) followed by a consolidation phase (to reduce fragmentation) are dwarfed by the cost of the subsidies and do not provide a compelling justification for doing so.

We explore a number of traditional rationales for industrial policy. We find limited evidence that the shipbuilding industry generates significant spillovers to the rest of the domestic economy (e.g., steel production, ship owning, and the labour market). Nor do we find evidence of industry-wide learning-by-doing (Marshallian externalities) or support for strategic trade considerations. In terms of the benefits to Chinese trade, the policy implemented in the shipbuilding industry may have lowered freight rates and boosted China’s imports and exports, though evaluating the associated welfare gains falls beyond the scope of this paper. Finally, it is worth noting that non-economic arguments, such as national security, military considerations, and the desire to be world number one (Grossman 1990), could be important in the design of this policy. Regardless of the motivation, our analysis provides cost estimates (and welfare losses) and information on the relative efficacy of implementing different policies that can be used as guidance for future policies.

To read the original report, click here

References

Baldwin, R E (1969), “The case against infant-industry tariff protection”, Journal of Political Economy 77(3): 295-305.

Barwick, P J, M Kalouptsidi and N Zahur (2019), “China’s industrial policy: An empirical evaluation”, NBER working paper 26075.

Grossman, G M (1990), “Promoting new industrial activities: A survey of recent arguments and evidence”, OECD Economic Studies 14.

Krueger, A O (1990), “Government failures in development”, Journal of Economic Perspectives 4(3): 9-23.

Rodrik, D (2010), “The return of industrial policy”, Project Syndicate, 12 April.

Yap, C-W and P Mazur (2013), “China aims to create electronic giants”, Wall Street Journal, 22 January.