The implementation stage of the African Continental Free Trade Area (AfCFTA) is due to begin in under three months. While the COVID-19 crisis has undoubtedly complicated the picture, the East Africa region is actually well-placed to implement the AfCFTA. Despite the skepticism expressed in some quarters about the ability of countries to get the landmark trade agreement up and running, there are strong reasons for optimism.

Thus far, it is true that only five countries in Eastern Africa have deposited their ratification of the AfCFTA. However, it is not the number of countries that counts but the fact that a regional block of contiguous countries—representing around three-quarters of regional GDP—is coalescing. From January 1, 2021, Djibouti, Ethiopia, Kenya, Rwanda, and Uganda will all begin a reduction in their tariffs—starting with a linear reduction on 90 percent of tariff lines—leading to the elimination of tariffs on intra-regional imports over a period of five years (10 years in the case of countries classified by the United Nations as “least developed countries”); by the standards of regional trade agreements, this pace of liberalization will be quite rapid.

Figure 1. East African countries that have deposited the ratification of the AfCFTA with the African Union, September 2020

Source: TRALAC, 2020

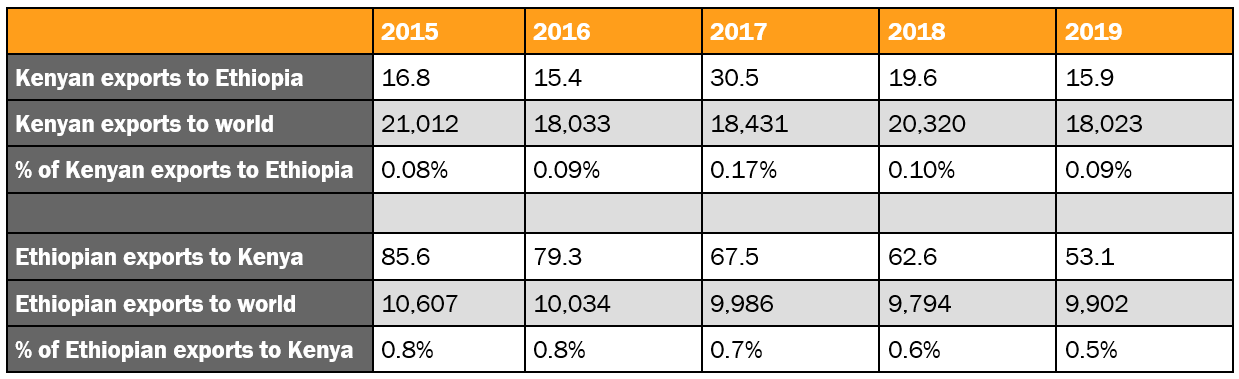

One of the big boons for the region from the AfCFTA will be unblocking the trade barriers between Kenya and Ethiopia—the two largest economies in eastern Africa. Despite previous efforts to deepen economic relations, the volumes of bilateral trade between the two remain exceedingly low. In fact, total bilateral trade did not even reach $70 million in 2019, accounting for just 0.5 percent of Ethiopia’s total exports and 0.09 percent of Kenya’s, and consisting principally of food and live animals and some manufactured goods (Table 1).

Table 1. Bilateral Ethiopian/Kenyan trade, 2015-2019 (millions USD and %)

Source: IMF Direction of Trade Statistics

The reasons for this neglect so far of these neighboring markets are fairly clear and go beyond the usual considerations of prevailing low per capita incomes. On the one hand, Ethiopia retains a fairly protectionist tariff policy, with high tariff peaks in particular sectors. But East African Community (EAC) members like Kenya (and not Ethiopia) also currently impose a high common external tariff on imports of Ethiopian goods in spite of the fact that both countries are members of regional grouping the Common Market for Eastern and Southern Africa (COMESA). The reason is that Ethiopia has not yet acceded to the COMESA Free Trade Area, and, hence, relatively high tariffs are still imposed on bilateral trade. A similar problem impacts Burundian, Rwandan, and Ugandan trade with neighboring Democratic Republic of the Congo (DRC)—all are members of COMESA, yet the DRC has yet to accede to the FTA.

In principle, the implementation of the AfCFTA will pave the way for a rapid dismantling of such impediments to cross-border trade. Alongside the removal of tariff barriers, the AfCFTA will also focus attention on outstanding nontariff barriers (NTBs), an important step toward increased trade in the region as studies consistently show that NTBs constrain intra-regional trade as much as or even more than tariff barriers. East Africa has already made some progress in this area by, for example, installing 25 one-stop border posts, significantly reducing the time taken for goods to pass through customs. Accompanying regional programs to the AfCFTA, like the African Union’s Action Plan for Boosting Intra-Africa Trade (BIAT), should help accelerate the progress.

To be sure, East Africa will continue to face a number of challenges, including one shared by all countries on the continent: the need to rapidly finalize the tariff offers and outstanding negotiations on the rules of origin as well as the schedules on services trade offers. This shared challenge will be particularly tough as the negotiations in areas like services and those in phase II such as competition and intellectual property policies will inevitably be quite complex and highly technical.

A second challenge is peculiar to the East African Community. Of the six members, only three have so far ratified the AfCFTA. Because the regional block of the EAC is a customs union and, consequently, has a common external tariff (CET), without further ratification of the AfCFTA by the other three member states, problems for the integrity of the CET will arise. Rules of origin in principle may limit this problem, but their liberal application will lead to greater bureaucratic overheads and increase the risk of trade diversion (whereby trade is diverted from a more efficient exporter toward a less efficient one because of the differential tariffs being applied). This could thereby reduce the benefits derived from the AfCFTA. Thus, the greater the degree of harmonization of trade policy regimes within East Africa, the better, as this will facilitate deeper regional economic integration and pave the way for the eventual formation of an African-wide customs union, as contemplated under the AfCFTA agreement.

A third related question is how to manage future trade negotiations with third parties. Mindful of the consequences of a possible phasing out of the African Growth and Opportunity Act (AGOA) in 2025, Kenya has already entered into negotiations with the aim of establishing a free trade agreement with the United States. Eager to establish new trade deals after its departure from the European Union, the United Kingdom is also approaching a number of countries in the region. The Kenya-U.S. free trade agreement has been particularly controversial, but perhaps unduly so: In principle, there is nothing impeding countries in East Africa from negotiating with third parties. However, for the reasons explained above with respect to rules of origin, it is better to avoid totally disparate approaches to third-party negotiations.

In short, to move forward decisively with AfCFTA implementation, East Africa needs to be better integrated both internally and with the wider African economy. However, it would be preferable, wherever possible, that national policy is aligned and that the regional blocks move together. By reenergizing existing commitments, such as those attained through COMESA and the EAC, or those envisaged under the Tripartite Agreement between SADC, COMESA, and the EAC, the AfCFTA will provide the perfect framework to achieve that goal.

Andrew Mold is the Chief, Regional Integration and AfCFTA Cluster, Office for Eastern Africa – United Nations Economic Commission for Africa.

To read the original blog, click here.