Intra-African trade is widely perceived as low compared to other regions of the world, an argument made ad nauseum in both academic and policymaking circles. Some observers are especially disparaging about its potential. One recent textbook on African economic development (Cramer et al., 2020:65) claims that:

“Despite decades of negotiations and agreements within subregions and RECs in Africa, intra-African trade remains a tiny proportion of the continent’s overall trade. … [While] greater intra-African trade may be rhetorically appealing on grounds of economic nationalism or South–South solidarity, as a blueprint for accelerated development it is a fantasy.”

We beg to differ and argue that intra-African trade has much greater economic significance than is commonly believed. The orthodox narrative is driven by three errors: 1) The comparisons made with other regional blocks are frequently misleading and do not compare like with like; 2) the picture of intra-African trade is distorted by large-scale commodity exports to destinations outside the continent; and 3) there is a systematic failure to recognize the scale of informal cross-border trade.

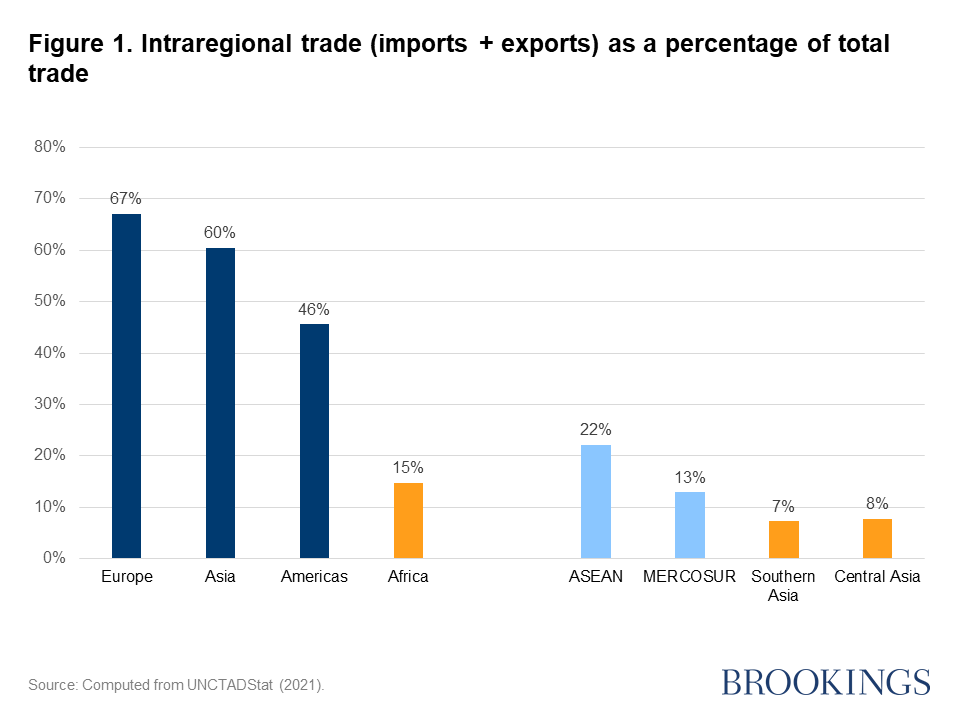

The African continent is often compared in a poor light vis-à-vis other continents in terms of the extent of intraregional trade. On a continental level, this argument, at first sight, seems true given the low percentage of intra-African trade of the region’s total trade (Figure 1). However, if we focus on subgroupings within these continental blocks, their intraregional trade figures are suddenly not so impressive. Compared to the Asian average, for instance, Central and Southern Asia are relatively less prosperous regions with less industrialized and diversified economies. Likewise, the ASEAN (Association of Southeast Asian Nations) grouping straddles countries with highly diverging levels of income and economic diversification—and with different types of economic integration into the global economy. For example, only 9 percent of Vietnam’s trade is currently with other ASEAN member states.

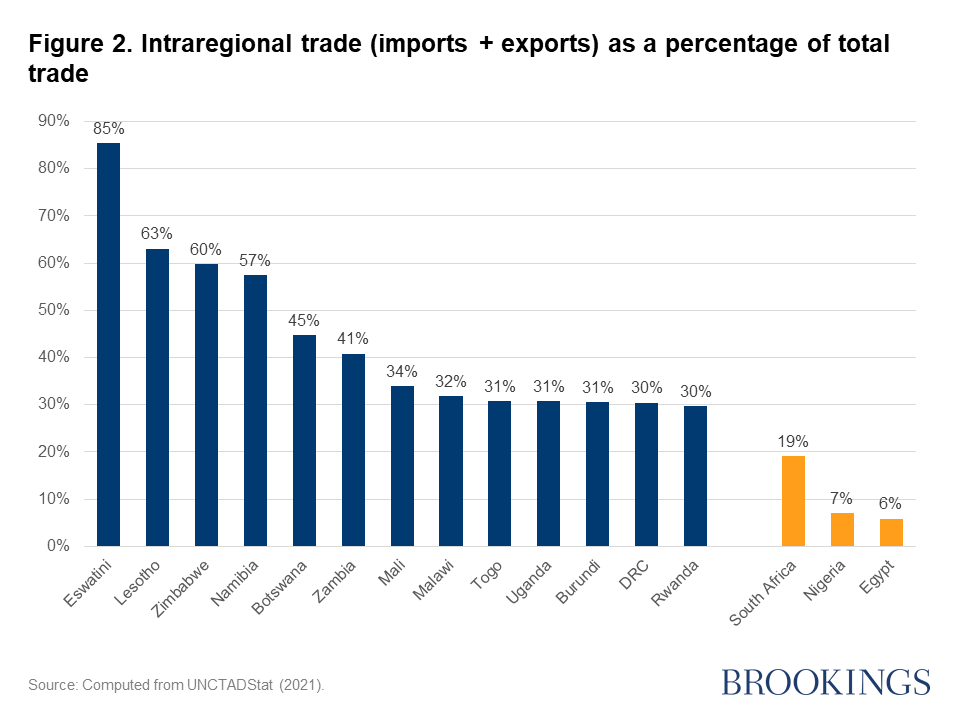

Conversely, in a similar breakdown of African trade figures, we find some subsets of African countries (particularly the landlocked ones) with significantly higher levels of dependence on intraregional trade than the continental average (Figure 2). In fact, what actually drags down the African average of intraregional trade are the continent’s larger economies—Egypt, Nigeria, and South Africa—distorting the picture of the importance of intra-African trade for the rest of the continent. For each of these countries, the reason for the low dependence on the African market varies: As a country with long-standing market access agreements with the European Union, Egypt has in the past prioritized the markets of its northern neighbors; for Nigeria, it reflects the country’s oil wealth; and for South Africa, there are historical reasons, related to its apartheid economy, that make its economy less dependent on its regional neighbors’ markets than would otherwise have been the case. The basic point is that many African countries have a higher dependence on the continental market than average figures denote.

The picture of intra-African trade is distorted by commodity exports to destinations outside the continent

The extreme dependence on commodity exports of a minority of African countries creates a misleading narrative around intra-African trade. This trend is a common characteristic of the patterns of trade in resource-rich regions: For example, after nearly three decades of existence, the share of MERCOSUR’s trade that is intraregional (see again Figure 1) is still lower than the African average. This outcome is largely because the bloc is dominated by one of the world’s largest commodity exporters—Brazil—and the principal demand for its commodities comes from outside the region. Africa finds itself in a similar situation: The region holds a significant proportion of global mineral reserves (e.g., 60 percent of manganese, 75 percent of phosphates, 85 percent of platinum, 80 percent of chrome, 60 percent of cobalt, and 75 percent of diamonds) and is responsible for nearly 10 percent of global oil and gas production. Notably, the bulk of these commodities are destined for markets outside Africa, dragging down the share of intraregional exports.

This structural feature very much distorts our vision of the potential of the continental market. Angola is a case in point: Oil comprises more than 90 percent of its exports—nearly all of which is destined to the United States. But strip out those extraregional commodity exports, and suddenly, according to our calculations (based again on UNCTADStat data), the importance of intra-African exports for Angola jumps to around three-quarters of the country’s total exports. It also needs remembering that while the continent is rightly considered as “resource-rich,” this is not true for the average African country, more than half of which are net commodity importers, not exporters. As a corollary of this, most African countries tend to have a higher dependence on the continental market than the principal commodity exporters.

There is a systematic failure to recognize the scale of informal cross-border trade

A final reason why our perception of intra-African trade is so distorted is the prevalence of informal trade. A lot of African borders are extremely porous; indeed, simply the length of borders inhibits against tight controls. While informal cross-border trade is a global phenomenon, studies tend to concur that it is more widespread on the African continent vis-à-vis other developing regions (e.g., FAO, 2020, Afreximbank 2020). Almost by definition, all informal trade is intra-African, implying once again that the real extent of intraregional trade is much higher than can be gleaned from official trade statistics alone.

Table 1 provides some estimates of the scale of informal trade relative to formal sector exports. With the exception of Tunisia (which has low formal-sector, intra-African exports), the smaller landlocked countries are usually where informal sector trade is most intensive. Summarizing the available data, Harding (2019) concludes that intra-African trade is systematically underreported by anything between 11 percent and 40 percent.

Conclusions and policy implications

The stylized facts described above have a number of important implications for policy, especially at a time when trading under the African Continental Free Trade Area (AfCFTA) has begun:

- Policies should be adopted to address the extensive barriers across the continent to informal cross-border trade (World Bank, 2020). Once fully implemented, the AfCFTA may see a sudden blooming of small-scale, cross-border trade, as the incentives for keeping informal sector trade off the record suddenly disappear.

- The impression of sluggish intra-African trade is wrong: It represents a high share of total African trade and is usually the more dynamic—and certainly the more diversified—element of a typical African country’s exports. This disarms the excessively simplistic but widespread myth that African countries have nothing to trade with one another.

- National trade strategies need to be consistent with these stylized facts—and prioritize intra-African trade rather than expend political capital in prolonged free trade agreement negotiations with extra-African trading partners.

Andrew Mold is chief, Regional Integration and AfCFTA Cluster, Office for Eastern Africa, United Nations Economic Commission for Africa.

Samiha Chowdhury is a consultant with the World Bank Group.

To read the original post by the Brookings Institute, please click here.